Forensic accounting is a specialized field of accounting that combines accounting, auditing, and investigative skills to analyze financial information for legal purposes. The primary objective of forensic accountants is to uncover and document financial fraud, embezzlement, or other financial irregularities. They play a critical role in legal proceedings, investigations, and dispute resolution.

Forensic accounting includes its role in discovering financial crimes, explaining the nature of these crimes to the courts, tracing funds, identifying assets, conducting asset recovery, and performing due diligence reviews.

In short, forensic accounting is dedicated to investigating and analyzing financial information to support legal cases in fraud investigations, dispute resolutions, and litigation.

Fig. 1: Forensic Accounting

Key Aspects of Forensic Accounting

Key aspects of forensic accounting include:

Investigation of Financial Irregularities: Forensic accountants investigate financial discrepancies, fraud, and other financial crimes within an organization or as part of legal cases.

Tracing and Identifying Financial Transactions: They trace financial transactions to identify any irregularities, misappropriations, or hidden assets. This often involves a detailed analysis of financial records and statements.

Fraud Prevention and Detection: Forensic accountants assist in developing and implementing measures to prevent and detect fraudulent activities within an organization. This proactive strategy enables businesses to protect their assets.

Quantifying Damages: Forensic accountants assess financial damages in cases of disputes, insurance claims, or legal conflicts. They use their expertise to calculate the financial impact of the alleged wrongdoing.

Dispute Resolution: Forensic accountants often work in alternative dispute resolution settings, providing financial expertise to help parties resolve conflicts outside of traditional court proceedings.

Litigation Support: They offer support to attorneys and legal teams by providing financial analysis, documentation, and expert advice during legal proceedings.

Ethical Considerations: Forensic accountants adhere to a high level of ethical standards in their work. They must maintain objectivity, integrity, and confidentiality, ensuring the information they uncover is handled responsibly.

Collaboration with Law Enforcement: Forensic accountants may collaborate with law enforcement agencies in cases involving financial crimes. They provide valuable insights and evidence to support criminal investigations.

Expert Witness Testimony: In legal proceedings, forensic accountants may be called upon to provide expert witness testimony. They present their findings clearly and understandably, helping the court understand complex financial matters.

When is Forensic Accounting needed?

Forensic accounting is needed in various situations where there are suspicions or evidence of financial misconduct, fraud, or when financial expertise is crucial for legal proceedings. Here are common scenarios that necessitate the involvement of forensic accountants:

Suspected Fraud or Embezzlement: When there are suspicions of fraudulent activities, misappropriation of funds, or embezzlement within an organization.

Financial Statement Irregularities: In cases where financial statements show irregularities, inconsistencies, or potential manipulation, prompting the need for a detailed investigation.

Dispute Resolution: During legal disputes, such as business or contractual disputes, where financial evidence is required to assess damages or resolve financial disagreements.

Insurance Claims Investigations: When there are suspicions of fraudulent insurance claims, forensic accountants are engaged to investigate and assess the validity of the claims.

Bankruptcy and Insolvency: In situations involving bankruptcy or insolvency, forensic accountants may be needed to trace funds, identify assets, and assess financial transactions to determine the financial condition of the business.

Employee Misconduct: When there are allegations of financial misconduct by employees, such as theft, bribery, or other forms of financial impropriety.

Mergers and Acquisitions: Before mergers or acquisitions, to conduct due diligence reviews and assess the financial health and integrity of the businesses involved.

Divorce Proceedings: In divorce cases where there are complex financial matters, forensic accountants may be engaged to analyze financial records, assess the value of assets, and determine spousal support.

Money Laundering Investigations: When there are suspicions of money laundering activities, forensic accountants may be involved in tracing funds, identifying financial transactions, and providing evidence for legal action.

Regulatory Compliance: In situations where organizations need to ensure compliance with financial regulations and prevent financial crimes.

Whistle-blower Allegations: In response to whistle-blower allegations of financial wrongdoing, forensic accountants may be brought in to investigate and validate claims.

Expert Witness Testimony: In legal proceedings where expert testimony on financial matters is required, such as fraud trials, breach of contract cases, or disputes requiring financial expertise.

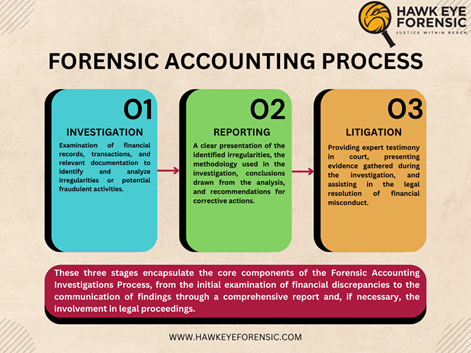

The process of Forensic Accounting

Forensic accounting typically involves three processes:

Investigation: Investigation involves the thorough examination of financial records, transactions, and relevant documentation to identify and analyze irregularities or potential fraudulent activities. Forensic accountants use various techniques and tools to gather evidence and build a comprehensive understanding of the financial situation.

Reporting: After completing the investigation, forensic accountants compile their findings into a detailed report. This document typically includes a clear presentation of the identified irregularities, the methodology used in the investigation, conclusions drawn from the analysis, and recommendations for corrective actions. The report serves as a crucial communication tool for stakeholders.

Litigation: In cases where the findings warrant legal action, the litigation stage involves collaborating with legal teams to initiate and support legal proceedings. This may include providing expert testimony in court, presenting evidence gathered during the investigation, and assisting in the legal resolution of financial misconduct.

Fig. 2. The process of Forensic Accounting

Challenges in Forensic Accounting

Some common challenges in forensic accounting include:

As technology advances, financial criminals become more sophisticated in their methods. Cybercrimes, hacking, and other tech-based frauds pose challenges for forensic accountants who must adapt to evolving techniques.

The sheer volume and complexity of financial data can be overwhelming. Forensic accountants often deal with extensive datasets, requiring advanced analytical tools and expertise to sift through the information effectively.

Balancing legal and ethical considerations can be challenging. Forensic accountants must navigate complex legal frameworks and adhere to ethical standards while conducting investigations.

Ensuring that the evidence gathered is admissible in court can be a challenge. Forensic accountants must follow proper procedures to maintain the integrity of the evidence and comply with legal standards.

Financial regulations and reporting standards evolve with time. Forensic accountants need to stay updated on changes in regulations to ensure their investigations are compliant and relevant.

Financial crimes often transcend borders. Investigating and prosecuting cases that involve international elements can be challenging due to jurisdictional issues and differences in legal systems.

Individuals or organizations under investigation may resist or obstruct the forensic accounting process. Obtaining cooperation and access to relevant documents can be challenging, hindering the investigative process.

Keeping pace with technological advancements is crucial. Forensic accountants must be proficient in utilizing advanced forensic tools and technologies to analyze digital data and detect electronic fraud.

Forensic accounting investigations can be resource-intensive. Limited budgets, time constraints, and other resource challenges may impact the thoroughness and scope of investigations.

The reputation of individuals or organizations under investigation can be damaged even if they are later found innocent. Forensic accountants must handle investigations with sensitivity to avoid unwarranted reputational harm.

Providing expert witness testimony requires clear communication and presentation skills. Forensic accountants may face challenges in conveying complex financial information to judges and juries in an easily understandable way.

Financial criminals constantly devise new schemes. Forensic accountants must stay vigilant and continually update their skills to recognize and investigate emerging fraud patterns.

Future aspect

As technology advances, the domain of forensic accounting transforms. The digital environment introduces fresh challenges and prospects for forensic accountants in uncovering and examining financial fraud.

Innovative technologies like blockchain and artificial intelligence are reshaping the recording and analysis of financial transactions. To proficiently investigate and prevent fraud in this digital era, forensic accountants must remain up to date on these developments.

Conclusion

In conclusion, the future of forensic accounting holds exciting prospects and challenges. As technology continues to advance, forensic accountants will harness tools like AI and blockchain to enhance investigative capabilities. The rise of cybercrimes and cryptocurrencies will necessitate expertise in cyber forensics. Collaboration on a global scale will become crucial to address cross-border financial crimes. Regulatory changes and a proactive focus on preventive measures will shape the landscape. Continuous professional development, specialization, and a commitment to ethical standards will be vital for success in this dynamic field. Forensic accounting, evolving with the times, remains a key player in maintaining financial integrity and combating financial crimes.

Honigsberg, C. (2020). Forensic Accounting. Annual Review of Law and Social Science, 16(1), pp.147–164. doi:https://doi.org/10.1146/annurev-lawsocsci-020320-022159

Cloud computing has become an important aspect of many organizations’ IT infrastructures, offering numerous advantages such as scalability, flexibility, and cost-effectiveness. However, the increasing use of cloud technology creates more ...

Post comments (0)